November 9, 2022

In

Articles, Design Leadership

Fintech uses Design but not in the way it should

I was honoured to be invited last Friday (4th Nov 2022) to speak at the Singapore Fintech Festival’s Talent Pavilion organised by our partner WSG (Workforce Singapore). I shared why Fintech needs Design. But before I get into that, let me share a few of my observations of the festival and my thoughts about Fintech in general.

Walking through all 6 halls of tech goodness, you could feel the buzz. Indeed there was a lot of hype for this festival, the first since the country reopened after COVID. However looking past the glam and glitter, there are a lot of problems. Many of which throwing more money at it, is not going to help solve. I can’t help but be reminded of the saying: “Drinking the Kool-Aid” which is something everyone did just before the 2000 dot-com bust.

I love technology. I’ve spent the last 25 years bringing all kinds of tech solutions to market. So I could see right away that this Fintech hype is no different to the journey of many of its predecessors. The latest Gartner Hype Cycle for 2022, published on 10th August 2022, is a nice starting point for our discussion.

As you can see above, many of the themes at the Fintech Festival: Web3, Blockchain, Metaverse, Artificial Intelligence (AI), and Decentralise Finance (DeFi) are estimated by Gartner to be 5-10 years out. As in 5-10 years before the tech is both productive and profitable through mass adoption. It was clear roaming the booths and chatting with exhibitors, that while everything looks great and “well designed”, it is not clear that many have a strong business case that can lead to financial sustainability beyond the initial VC investment.

As someone who closely watches, trades and “invests” in NFTs, this “trough of disillusionment” is closer than you think. During this phase in the Hype Cycle: “Interest wanes as experiments and implementations fail to deliver. Producers of the technology shake out or fail. Investment continues only if the surviving providers improve their products to the satisfaction of early adopters.” There is a reason why people have stopped spending hundreds of thousands on pictures of bored apes or portraits with random clothing accessories.

Interestingly, there is also very little differentiation between each company. They seem to be all doing the same thing. It’s another payment portal/funds transfer/digital wallet, or crypto asset management/trading platform. I observed that many exhibitors were also not willing to explain exactly what they did or what made them different from the other platform next door. Sharing a similar experience with a colleague who also went to the event, she suggested that “perhaps they don’t even know themselves.”

The value proposition of Fintech is still not clear. Until this is clear, it is not going to have a mass adoption that will deliver financial sustainability. Currently, it’s all focused on what the tech can do, not how it will benefit the man on the street.

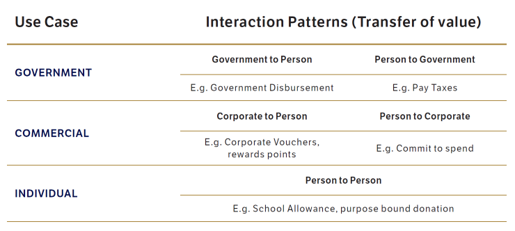

One organisation bucking this tech-focused trend is the Monetary Authority of Singapore (MAS). They are exploring the creation of a Retail Central Bank Digital Currency (CBDC) and prototyping potential scenarios of how it can be used. Their Project Orchid initiative looks at an application for CBDC in a form of Purpose Bound Money (PDM) that builds on the concept of programmable payment and programmable money. Nicely explained by the gentleman in the booth, “if I want to make sure my son spends his pocket money on a healthy lunch rather than toys, this is the tool for me.”

In wonderful Design Thinking fashion, rather than spend money and time building the ledger or tech stack, like many of the exhibitors in the festival, the MAS took a user-driven approach. They prototyped this idea by representing the PBM with digital vouchers (basically coupons) and then mass-testing these vouchers with the public, banks and retailers. Subsequent phases will explore optimal ledger technology and how it will integrate with existing financial market infrastructure (the key to mass adoption).

Source: MAS Project Orchard Report (Yes I know, it’s still all tech, but at least you know what the benefit of this tech is!)

It was also explained to me that MAS has assessed that there is no urgent need for a retail CBDC in Singapore at this point. So this bottom-up approach to learning will allow the MAS to understand what it will take to get Singaporeans on board a CBDC system as well as advance the financial infrastructure in Singapore.

Anyways going back to the topic of my talk, Fintech needs Design. We know in eCommerce, Fintech’s predecessor, that bad design causes an approximate loss of $18 billion in yearly revenue and $4 trillion worth of merchandise abandoned in digital carts next year alone. So you need Design, not just in creating great digital products (ie great UX/UI), but as a strategic tool to:

- understand a user’s needs and “Jobs To Be Done” and how your technology can assist them to reach goals. (Just what is Fintech’s JTBD anyway?)

- bridge the gap in the user’s understanding of the tech. (Use stories and narratives that are familiar to the user.)

- be empathic and understand a user’s resistance to change. (How can you create a great change management process to convince adoption?)

- and finally, link the experience across multiple touch-points from the brand, product, service, and space. (Last I checked, most people still live in the real world.)

Kudos to all the people involved in the festival, but I just wished I saw more examples of these 4 points as I roamed the halls. That’s all from me, but please feel free to share your thoughts in the comments below. Love to hear them!

No Comments